Index Funds and the Future of Corporate Governance: Theory, Evidence, and Policy

Working Paper Author/Authors

Abstract

Index funds own an increasingly large proportion of American public companies. The stewardship decisions of index fund managers—how they monitor, vote, and engage with their portfolio companies—can be expected to have a profound impact on the governance and performance of public companies and the economy. Understanding index fund stewardship, and how policymaking can improve it, is thus critical for corporate law scholarship. In this Article we contribute to such understanding by providing a comprehensive theoretical, empirical, and policy analysis of index fund stewardship.

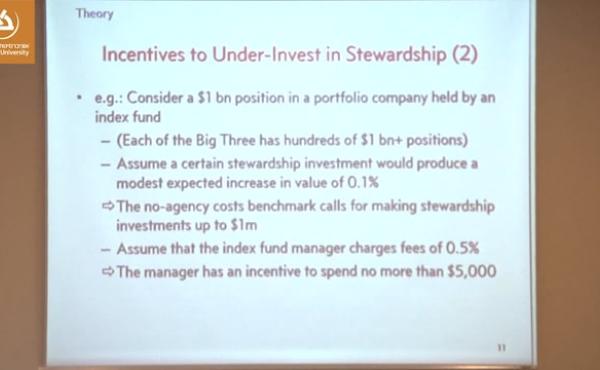

We begin by putting forward an agency-costs theory of index fund incentives. Stewardship decisions by index funds depend not just on the interests of index fund investors but also on the incentives of index fund managers. Our agency-costs analysis shows that index fund managers have strong incentives to (i) underinvest in stewardship and (ii) defer excessively to the preferences and positions of corporate managers.

We then provide an empirical analysis of the full range of stewardship activities that index funds do and do not undertake, focusing on the three largest index fund managers, which we collectively refer to as the “Big Three.” We analyze four dimensions of the Big Three’s stewardship activities: the limited personnel time they devote to stewardship regarding most of their portfolio companies; the small minority of portfolio companies with which they have any private communications; their focus on divergences from governance principles and their limited attention to other issues that could be significant for their investors; and their pro-management voting patterns.

We also empirically investigate five ways in which the Big Three could fail to undertake adequate stewardship: the limited attention they pay to financial underperformance; their lack of involvement in the selection of directors and lack of attention to important director characteristics; their failure to take actions that would bring about governance changes that are desirable according to their own governance principles; their decision to stay on the sidelines regarding corporate governance reforms; and their avoidance of involvement in consequential securities litigation. We show that this body of evidence is, on the whole, consistent with the incentive problems that our agency-costs framework identifies.

Finally, we put forward a set of reforms that policymakers should consider in order to address the incentives of index fund managers to underinvest in stewardship, their incentives to be excessively deferential to corporate managers, and the continuing rise of index investing. We also discuss how our analysis should reorient important ongoing debates regarding common ownership and hedge fund activism.

The policy measures we put forward, and the beneficial role of hedge fund activism, can partly but not fully address the incentive problems that we analyze and document. These problems are expected to remain a significant aspect of the corporate governance landscape and should be the subject of close attention by policymakers, market participants, and scholars.

This paper is part of a larger project on the incentives of investment managers that also includes The Agency Problems of Institutional Investors (with Alma Cohen) and The Specter of the Giant Three.